I have completed more than fifteen Title Split projects. The mistakes I describe below are not theoretical. Each one is something I have either seen compress a margin to nothing, or something I avoided only because the due diligence process was designed specifically to catch it.

1. Buying the wrong lease structure

The most expensive mistake is made at the point of acquisition. An operator buys a property with an existing lease that looks conventional, only to discover later that the lease terms prevent the intended division. Ground rent escalators, restrictive covenants, service charge mechanisms and alienation clauses can each render a Title Split impossible or uneconomic.

At Inspired Property Group, every acquisition begins with a lease review by a solicitor who has handled Title Split transactions before. Not after the offer. Before it.

2. Assuming the lender will understand the strategy

Most lenders have never financed a Title Split. The ones that have do so under specific product terms with clear qualification criteria. Walking into a branch and describing the strategy in layman's terms is not a viable approach. The lender will either decline or offer terms that assume a risk profile the project does not actually carry.

We maintain relationships with a panel of lenders who have explicitly approved Title Split transactions. The financing structure is agreed in principle before the asset is sourced, not after.

3. Underestimating the HM Land Registry timeline

The registration of new titles at HM Land Registry is not a predictable process. In our experience, straightforward applications can be processed in weeks. Complex ones, or applications submitted during peak periods, can take months. An operator who has modelled their return on a four-week registration and then waits fourteen weeks has a cash flow problem.

Our underwriting assumes the longest reasonable timeline. If the registration completes sooner, the return improves. If it does not, the project remains viable.

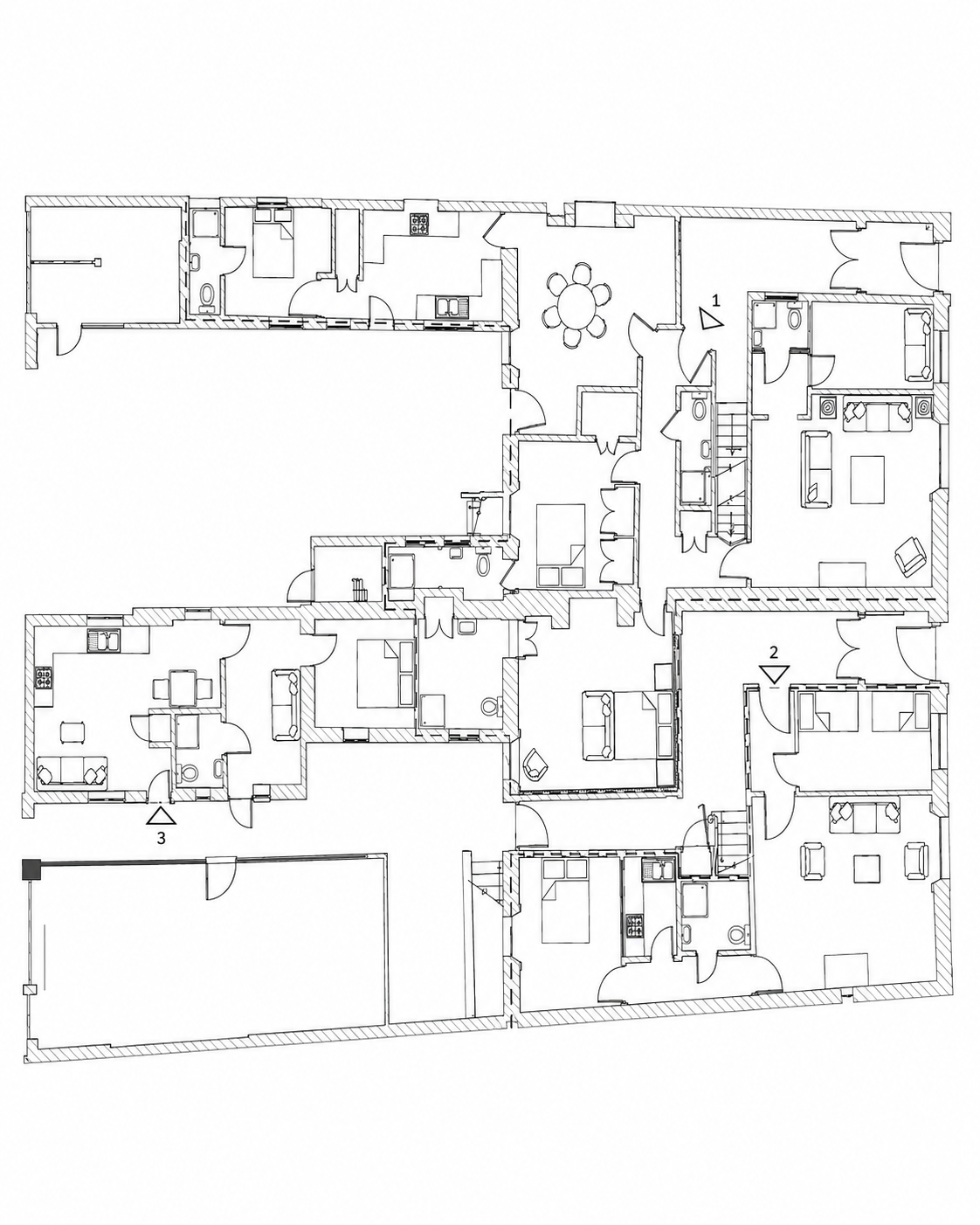

4. Poor unit configuration

The division of a building into separate units is not simply a matter of drawing lines on a floor plan. Each unit must be independently habitable, separately metered, and capable of being valued on its own merits. A unit that shares a hallway in a way that creates ambiguity about maintenance liability, or a unit with an awkward access arrangement, will be penalised by the valuer.

We engage the surveyor at the planning stage, not at the valuation stage. The unit configuration is designed around the valuer's methodology, not adjusted to fit it afterwards.

5. Inadequate lease drafting

The leases that govern the relationship between the freeholder and the individual leaseholders are the legal foundation of the entire structure. A lease that is ambiguous on service charges, repairs, insurance, or forfeiture creates the conditions for future disputes that can destroy value.

Our leases are drafted by solicitors who specialise in this work. They are not adapted from standard templates. The cost of proper drafting is material. The cost of inadequate drafting is usually the entire margin.

6. Treating each project as a one-off

An operator who treats each Title Split as an isolated transaction never builds the advantages that come from repetition: the settled solicitor, the surveyor who understands the methodology, the lender who has seen the structure before, the sourcing filter that eliminates unsuitable properties in seconds. Each project starts from zero.

This is the primary reason we concentrate exclusively on this strategy. The compounding benefits of repetition are, in our experience, as valuable as the uplift on any individual project.

7. Failing to underwrite to stand-alone economics

The most dangerous assumption in property is that the market will bail you out. An operator who underwrites to optimistic rents, generous refinance valuations, or favourable market movements is not underwriting at all. They are speculating.

Our underwriting assumes the worst reasonable outcome in each variable. The project must be viable on those terms. Any upside from market movement, rental growth, or refinancing generosity is treated as a bonus, not as a component of the expected return.

What I would add

There is an eighth mistake, less common but more consequential: working with the wrong investor partners. A Title Split is a technically demanding, timeline-sensitive structure. An investor who does not understand the strategy, who requires constant reassurance, or who treats the project as a liquid position will create friction that can be as damaging as any legal error.

We are selective about our partners for the same reason we are selective about our projects. The right structure with the wrong capital is the wrong structure.