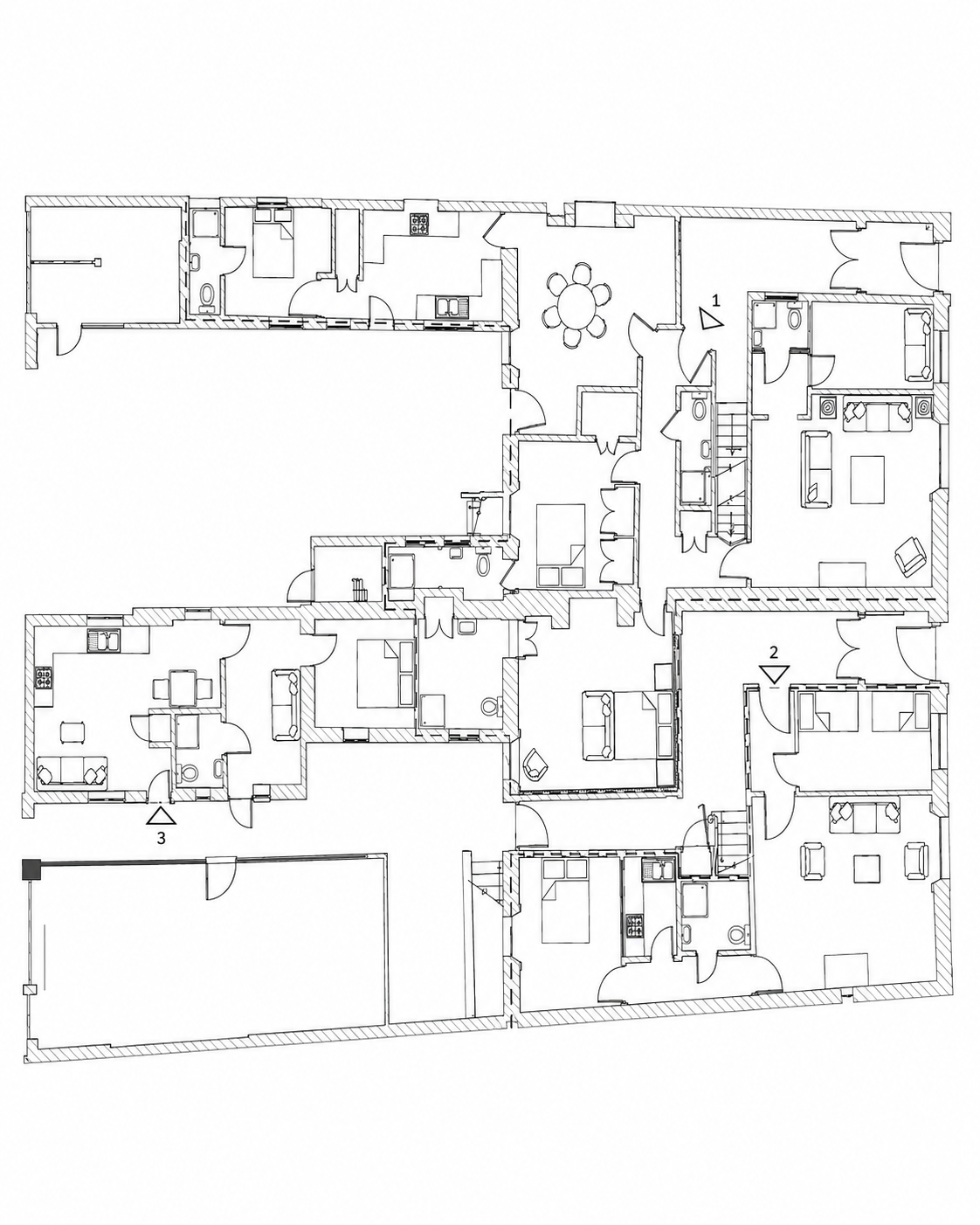

The short definition

A Title Split is the legal subdivision of a single registered title at HM Land Registry into two or more separate titles, each capable of being independently sold, mortgaged and occupied. In a typical UK project, a freehold building that contains several self-contained units — flats above a shop, a converted townhouse, a small block — is restructured so that each unit is held under its own leasehold title, with the freehold reversion held separately.

That is the strategy in one sentence. Everything that follows is the detail that explains why it works, why it is defensible, and why most investors who attempt it without a specialist team find the project takes longer and costs more than they planned.

Where the uplift comes from

A single freehold containing multiple units is almost always valued on an investment basis — as a yielding asset, capitalised at a commercial yield. That is the right valuation methodology for what the asset legally is at the point of acquisition: one title, producing a rental income.

Once each unit holds its own leasehold title, the asset has changed categories. Each unit is now individually saleable to an owner-occupier or to a single-unit landlord, and each is valued on a residential comparable basis — by reference to what similar one- or two-bedroom units in the same street and the same condition have recently sold for.

The structural uplift in a Title Split is the gap between those two valuation methodologies. The market is not being asked to move. The asset's legal status has been moved into alignment with how the market already values comparable stock.

What a Title Split is not

It is worth being precise about what a Title Split is not, because the strategy is regularly confused with adjacent activities that carry very different risks.

- It is not planning gain. A Title Split does not require planning permission. The units already exist as self-contained dwellings; the work is legal, not planning-led.

- It is not a refurbishment-led BRRR. Light cosmetic work may be done to support the individual sales, but the headline uplift is not produced by the refurbishment valuation. It is produced by the change in title.

- It is not a market bet. The exit is broader and less concentrated than for a single large investment property, because the resulting units appeal to owner-occupiers and small landlords rather than only to portfolio investors.

The process, end to end

A Title Split project is, at heart, a sequenced series of professional instructions. Done well, it is uneventful. Done badly, each missed step extends the timeline and erodes the margin. The headline stages are:

- Sourcing and screening. Filtering candidate properties by tenure, configuration, restrictive covenants and local comparable evidence. Most opportunities are rejected within minutes.

- Title and legal due diligence. A specialist solicitor reviews the existing title, restrictions and any charges to confirm that a clean split is achievable.

- Lender engagement. Existing charges over the original title must be released, varied or refinanced cleanly. A lender that will not cooperate is replaced before exchange, not after.

- Leasehold drafting. Individual leases are prepared to a standard that the residential conveyancer on the other side will accept on the eventual sale.

- HM Land Registry applications. The new individual titles are applied for and registered. This is the moment the structural uplift crystallises.

- Individual sales or refinance. Units are sold individually to owner-occupiers or small landlords, or refinanced on their new individual valuations.

Why it remains a specialist activity

On paper, any UK property investor could attempt a Title Split. In practice, it remains the preserve of a small number of operators for entirely practical reasons.

It rewards repetition. The professional team — solicitors who have drafted the leases dozens of times, surveyors who understand the valuation impact, planning consultants where required, lenders who recognise the structure — exists, but it is not the panel a generalist investor would assemble. It requires a sourcing discipline that screens out most opportunities before any time is spent. And it requires a tolerance for transactions that, by design, should look uneventful from the outside.

Is it right for an investor?

The useful question is not whether Title Splitting produces the highest possible return in any given year. In some years, it will not. The useful question is whether it produces an acceptable return without requiring the investor to take a view on the wider market.

For family offices, sophisticated private investors and joint-venture partners whose existing portfolios already carry meaningful exposure to market direction — through equities, through trading property, through development — that characteristic is precisely what earns Title Splitting a place in the allocation. It is not a thesis. It is a structure.